This article is the second in a three-part series about Zcash marketing strategy and perspectives. I invite you to look back at the 2018 Year in Review post and to look ahead with me as our 2019 marketing approach is introduced next week. Each quarter I will provide an update on my perspective about the market and the evolution of Zcash.

Our strategy

While the industry-wide prices and transactional activity have been low, development and investment in cryptocurrency infrastructure has been at an all-time high.

Large incumbents like Facebook and Microsoft have been building teams and projects, and well-regarded talent is leaving Silicon Valley companies to participate in blockchain projects. At Zcash Company, we have operationalized and animated some of the most advanced cryptographic research in the world. This work on zero-knowledge cryptography is now inspiring the creation of new companies and new ideas, focused on new use cases.

Massive amounts of money are flowing into the space, into new financial railroads — as evidenced by the $300M raise by Coinbase in October — and from large institutional investors and companies setting up global trading desks, including Galaxy, Cumberland, Circle and now Fidelity.

Tagomi Holdings has launched prime brokerage services for institutional investors, and the Intercontinental Exchange, the owner of the NYSE, has partnered with Starbucks and Microsoft on an exchange called BAKKT to help bring Bitcoin to the masses.

But really, we are in very early days. The foundations of the internet were created years before the advent of the “World Wide Web” and the pervasive use of browsers in the early 90s. We used telnet, ftp, usenet and gopher long before we had commercial browsers that allowed us to safely navigate content and commerce. Navigating the internet was too complicated for most people before the browser. We’re at a similar tipping point with cryptocurrencies as the technology becomes more usable to more people. It’s still too complicated right now, and the mental load is too high.

We have not reached critical mass, and we likely won’t until we mature across a number of complementary and parallel vectors, including technology, user experience, protocol governance, regulatory clarity, financial infrastructure and technology infrastructure.

In addition to all the aforementioned, I posit that we also must mature through currency adoption vectors. See Vijay Boyapati’s, “The Bullish Case for Bitcoin.” for a good overview on the evolution of money.

Currency adoption vectors

Currency adoption vectors represent first-order use cases for a currency. Other use cases exist for different types of blockchain projects (e.g., securities, non-fungible tokens, etc.). Those are not relevant for Zcash. Second-order use cases (e.g., smart contracts, messaging) have also been excluded for now. The four core adoption vectors are:

Speculative asset (SA): An asset with high risk and volatility relative to other assets. This may include trading without regard for the underlying fundamentals, but may also include early-stage investments.

Store of value (SoV): A store of value is an asset that maintains its value without depreciating relative to alternatives. First-order properties of a store of value include:

- Secure: The asset is safe from loss, and the owner is protected through privacy.

- Censorship resistant: A third party cannot prevent the owner from accessing or using the asset.

- Compliant: The owner is able to remain in good legal standing within their legal jurisdiction.

- Durable: The asset cannot be easily destroyed.

- Portable: The asset must be relatively easy to store and transport.

- Fungible: Individual units of the asset are interchangeable.

- Other secondary desirable properties: Divisible, scarce, established

Medium of exchange (MoE): An intermediary instrument used to facilitate the sale, purchase or trade of goods between parties. For an instrument to function as a MoE, it must represent a standard of value accepted by all parties.

Unit of account (UoA): The basis for which things are valued and bought or sold. For example, today a vendor might price an item in Zcash based upon the value of an underlying fiat currency, as their business is managed (profit and loss) in that underlying currency. In this case, the fiat currency is the UoA.

With Zcash, no currency-adjacent vector stands alone. It has the potential to support each one. The adjacencies are interdependent.

- Each vector produces a complementary network effect to its adjacent vectors.

- Each vector must reach some level of maturity before the subsequent vector will gain traction.

- Speculators, though not necessarily aligned with the Zcash vision, aren’t evil and are an important part of our ecosystem. They provide liquidity and awareness to support SoV.

- The speculative investor’s hope that an asset will be considered a SoV leads to increased adoption, which it turn provides a positive outcome for both SA and SoV use cases (Nash Equilibrium).

- SoV is symbiotic with MoE. As SoV matures and price fluctuations stabilize, an SoV asset becomes a safe and viable means to purchase goods and services.

- As an MoE is adopted broadly, it is used more consistently as a UoA, where both buyer and seller think about prices in that currency first.

Complementary vectors

In addition to technology adoption and the currency adoption vectors, other complimentary vectors must mature. Some are further along than others, but all must exist to gain mainstream adoption.

- Protocol governance: Determining which distributed governance models will prove to be both effective for innovating and ensuring safety.

- Regulation: Including regulatory recognition, education, frameworks and guidance within and across nations.

- User experience: The technology to support a positive user experience and reduce friction points.

- Financial infrastructure maturity: Liquidity, validation of the asset class, derivatives and tools.

- Technical infrastructure: Including privacy and scalability.

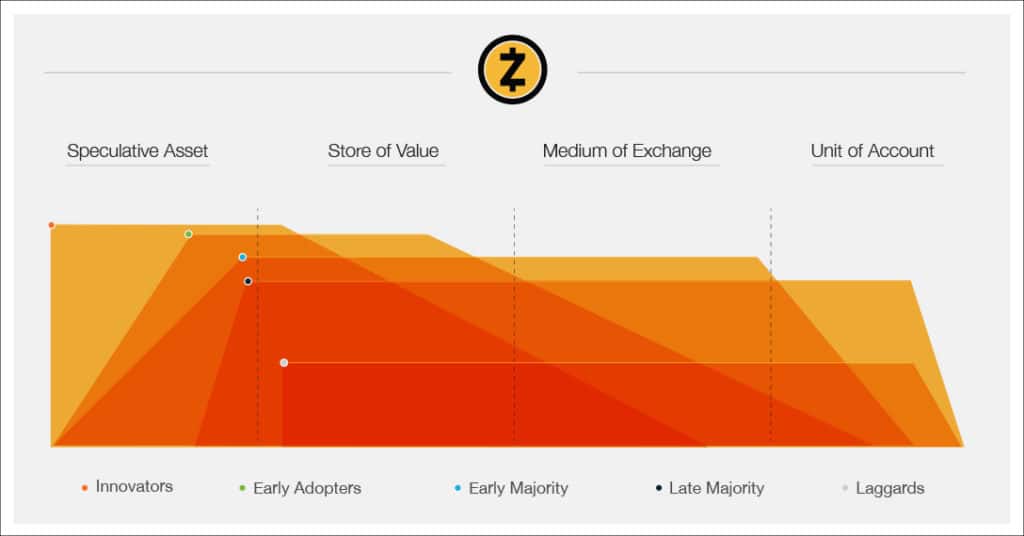

If we map categories of adopters (as indicated in the adoption curve graphic above) against currency adoption vectors, we get something like the diagram below, illustrating that early stages of technology adoption are better suited toward different use cases. For example, innovators are more likely to hold Zcash as a speculative asset than use it as a true MoE (though some claim to be living off Bitcoin), simply because there aren’t many places to use it as an MoE and the user experience is still painful. However, as the technology improves and other vectors mature, so too does the potential for use as MoE.

MoE hurdles

“…a monetary good will only be suitable as a medium of exchange when the sum of the opportunity cost and the transactional cost of using it in exchange drops below the cost of completing a trade without it.” – Vijay Boyapti

The reality is that Zcash (or any cryptocurrency) is not fully ready to be used broadly as a MoE for the following reasons:

- We are still in the Early Adopter phase and have not yet achieved adoption as a SoV.

- Usability for day-to-day transactions is insufficient (wallet usability, transaction confirmation times).

- Access to Zcash largely requires fiat on-ramps with a high degree of friction.

- Zcash doesn’t yet scale for broad MoE.

- Regulation is unclear and globally inconsistent. SoV is much more palatable, even if all parties recognize it as a Trojan horse.

- Taxation on spending is cumbersome and not fully defined.

- There is insufficient adoption and not enough options for earning or spending Zcash.

- Even early adopters are not sufficiently educated on cryptocurrencies and Zcash.

- The product market fit is still assumed and not proven beyond niche cases.

The regulatory vector

Regulators are trying to balance consumer protection (privacy) with their access to information. What most people haven’t realized is both goals are supported by regulated exchanges like Gemini and Coinbase should they implement Zcash shielded addresses. Encrypting the transactions sent or received by a regulated exchange does not prevent the regulators from seeing the contents of the transactions, but does prevent unauthorized third parties from doing so. It’s like turning on HTTPS instead of HTTP on your web site.

And yet, some people seem to be afraid of it. They are afraid that it will be used to traffic drugs and evade taxes. But I think that will change. The NSA tried to stop the widespread adoption of cryptography on the internet in the 1980s. Now the US Government mandates all its sites use https, this very encryption, to protect itself and its citizens.

Likewise, I believe that governments should and will eventually enforce privacy between regulated exchanges and cryptocurrency users. Those exchanges, like a bank, can enforce KYC/AML while protecting their citizens from bad actors or foreign governments that may be collecting data on their citizens. The regulatory perspective will move from fear to acceptance to recommended to mandated.

Summary

Cryptocurrency adoption is going viral but not yet mainstream. Non-speculative use is still the primary use case, and we have been quickly building the infrastructure to support cryptocurrencies as speculative assets with large exchanges like Coinbase, Gemini and Binance.

As liquidity and credibility build, the asset class will move beyond a speculative asset and into use as a Store of Value, or “digital gold,” because of its inherent first-order properties, and because tools, such as well-supported custodial solutions, will be available. And I believe regulation will be there to support it.

Once all this occurs, assuming the other vectors have kept pace, we’ll one day be able to use it, as a medium of exchange, at scale. Someday it could be used as a Unit of Account, but that remains a long way off.

The current state of the market and the thinking outlined in this post have been used to create the foundation of our 2019 GTM strategy. Stay tuned for the final post in this series, our 2019 Go-to-Market, which will be published on this blog next week.